The article is intended for car insurance product managers who want to understand how a beacon works, its advantages over traditional telematics devices, and the specific business cases that require combining a beacon with a mobile telematics app.

Introduction

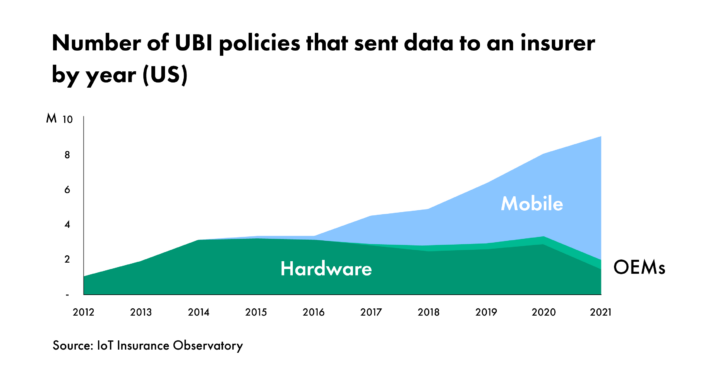

A study published by the IoT Insurance Observatory, a leading think tank on insurance innovation, reveals that insurers in the US have been increasingly using smartphone to collect driving data. All the alternative technologies, from connected boxes to connected vehicles, have experienced a downward trend since 2020.

While mobile‑based connected insurance is gaining traction in the US, its adoption in Europe has not generated the same enthusiasm. Most connected programs in the EU focus on very specific segments, such as young drivers and low‑mileage drivers (learn more in the Guide to Connected Insurance).

Past failures with telematics boxes and limited technical understanding of smartphone telematics benefits lead many EU insurers to hesitate before deploying large‑scale connected programs, despite the fact that most concerns can be resolved simply by adding a beacon to the app.

What is a beacon?

A beacon is an electronic device that emits a Bluetooth Low Energy (BLE) signal, consisting of a universal unique identifier (UUID), a major and a minor. The signal emits within a range of one to several dozen meters, and follows the iBeacon standard designed by Apple in 2013.

The main benefit of a beacon is that it can be easily detected by any iPhone or Android smartphone. When the telematics app detects the beacon's ID, and that an action in response to the detection of this ID has been programmed into its code, the app triggers the action, even when running in the background.

Vehicle identification and privacy

A mobile telematics SDK automatically records trips - without requiring a beacon (refer to the guide How does automatic trip detection work? for more details).

However, in Pay-As-You-Drive (also called pay‑per‑mile) insurance programs, as the premium depends on the distance driven, pairing the mobile app with a beacon makes sense as it gives the insurer certainty that the vehicle used is the one covered by the policy.

The beacon functions as a trigger: when the telematics app detects a trip without detecting the beacon’s signal, it infers that the policyholder is not in the insured vehicle. Therefore, it does not record the trip to preserve privacy.

Short trip detection

Without a beacon, the initial meters of a trip may not be analyzed because the telematics app requires a brief confirmation period to detect that the vehicle is indeed moving.

As a result, short trips under a few hundred meters may not be analysed by the telematics SDK. To capture every trip, even the shortest ones, insurers can pair the mobile application with a beacon. When the mobile app detects the beacon's signal, it triggers the trip analysis - ensuring the entire trip is analysed.

Distribution and lifespan

A beacon delivers a smooth and universal customer experience:

-

The beacon can be mailed to the policyholder with no pre‑configuration needed.

-

The policyholder links the beacon to the app and then places it beacon in the glove box.

-

The beacon is powered by standard AAA batteries. It has a lifespan of around 4 to 5 years. The policyholder simply needs to replace the batteries to extend the beacon’s lifetime.

Supply and cost

Unlike telematics boxes, which are complex technical devices, the beacon is both simple and generic. It has no microcontroller, no memory, and transmits no data. Its signal serves only one purpose: to indicate its presence to a mobile application.

A beacon is easy to manufacture and inexpensive. Many suppliers produce them. This allows insurers to keep costs under control and secure their supply chain.

|

How telematics boxes work? Telematics boxes, involve retrieving, processing, storing and transmitting information from the vehicle. The data can be transmitted via :

|

Conclusion

Benefiting from its technical simplicity, the beacon turns the telematics app into a solution that covers all the use cases of traditional telematics devices while delivering undeniable advantages:

-

A universal, generic technology that can equip any driver without distinction,

-

A smooth and consistent customer experience,

-

A simple and secure supply‑chain process,

-

Low‑cost distribution,

-

A longer lifespan.

Launching and scaling a connected insurance program relies on two key factors: optimizing driving data collection and reducing technology costs. The combination of a telematics app and a beacon is the only telematics solution that matches the performance of traditional devices while delivering a drastic cost reduction for insurers.